Allstate Says Broadcom Audited It Because It Left VMware: What Every Enterprise Should Learn

Executive Summary

In December 2025, VMware (a Broadcom subsidiary) filed a federal lawsuit in the Northern District of California accusing Allstate Insurance Company of obstructing a contractual software licensing audit and failing to maintain required records. Allstate responded in June 2026 that the audits—covering Tanzu, VMware, Agile Operations, and Mainframe products—were initiated only after it became clear the insurer would not renew contracts with VMware or sister company CA Technologies following Broadcom’s 2023 acquisition.

Allstate, a long-time VMware customer since 2008, claims it substantially complied in good faith, removed all VMware instances by September/October 2025, and declared the audit complete. Broadcom/VMware maintains that Allstate stonewalled the process, withheld materials, and breached explicit audit rights in its enterprise license agreements. Separate CA-related claims center on a business divestiture notification issue. Both matters remain ongoing as of July 2026, with alternative dispute resolution unsuccessful and dispositive motions deadlines proposed for May 2027.

This is not legal advice. This article analyzes publicly reported facts and broader infrastructure strategy implications. It does not speculate on litigation outcomes or offer opinions on contractual merits.

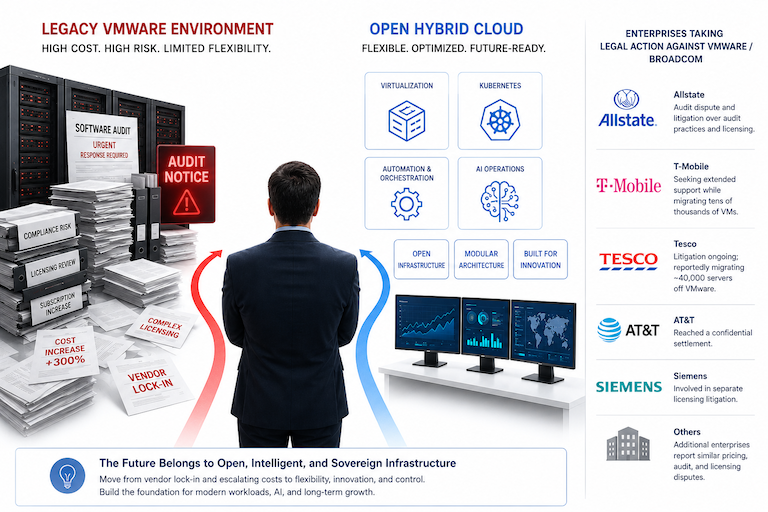

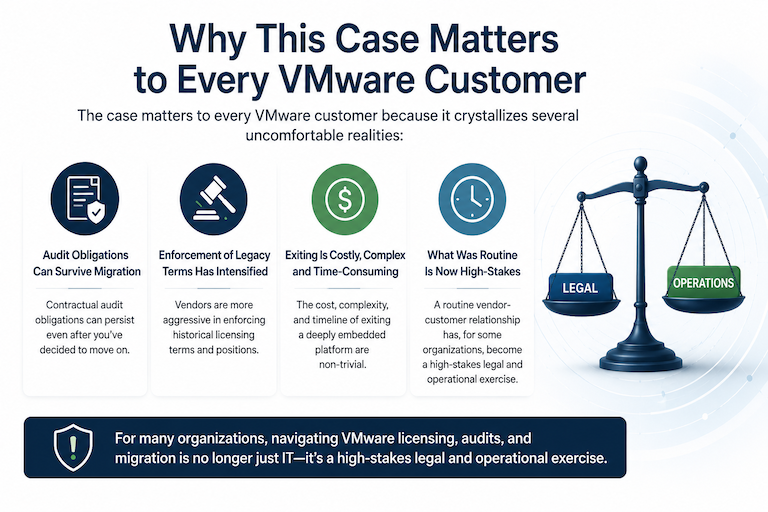

The case matters to every VMware customer because it crystallizes several uncomfortable realities: contractual audit obligations can survive migration decisions; vendor enforcement of legacy licensing terms has intensified; and the cost, complexity, and timeline of exiting a deeply embedded virtualization platform are non-trivial. What was once a routine vendor-customer relationship has, for some organizations, become a high-stakes legal and operational exercise.

Timeline of Events

A clear chronology helps separate fact from narrative.

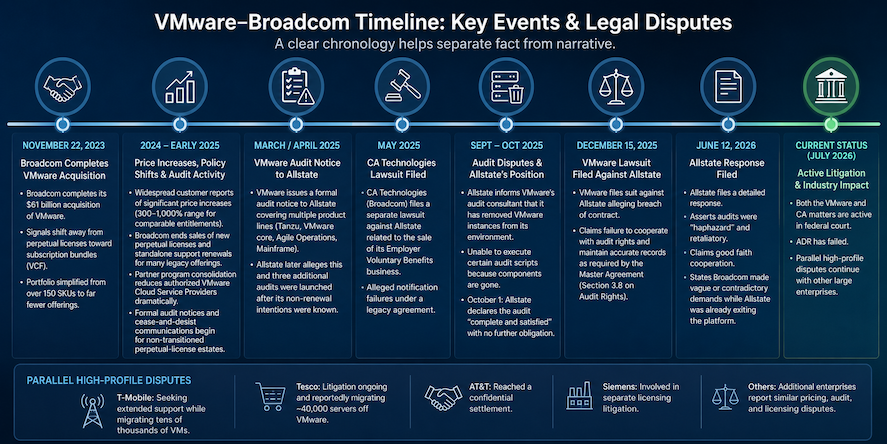

November 22, 2023 — Broadcom completes its $61 billion acquisition of VMware. Almost immediately, the company signals a shift away from perpetual licenses toward subscription bundles (notably VMware Cloud Foundation / VCF) and simplifies a portfolio that once contained over 150 SKUs into far fewer offerings.

2024 – Early 2025 — Widespread customer reports emerge of significant price increases (commonly cited in the 300–1,000% range for comparable entitlements). Broadcom ends sales of new perpetual licenses and standalone support renewals for many legacy offerings. Partner program consolidation reduces the number of authorized VMware Cloud Service Providers dramatically. Formal audit notices and cease-and-desist communications begin appearing for customers still running significant perpetual-license estates who have not transitioned to the new subscription model.

March/April 2025 — VMware issues a formal audit notice to Allstate covering multiple product lines (Tanzu, VMware core, Agile Operations, Mainframe). Allstate later alleges this and three additional audits were launched after its non-renewal intentions were known.

May 2025 — CA Technologies (Broadcom) files a separate lawsuit against Allstate related to the sale of its Employer Voluntary Benefits business and alleged notification failures under a legacy agreement.

September–October 2025 — Allstate informs VMware’s audit consultant that it has removed VMware instances from its environment and can no longer execute certain audit scripts because the components are gone. On October 1, Allstate declares the audit “complete and satisfied” with no further obligation.

December 15, 2025 — VMware files suit against Allstate alleging breach of contract, specifically failure to cooperate with audit rights and maintain accurate records as required by the Master Agreement (Section 3.8 on Audit Rights).

June 12, 2026 — Allstate files a detailed response asserting that the audits were “haphazard” and retaliatory, that it acted in good faith, and that Broadcom made vague or contradictory demands while Allstate was already exiting the platform.

Current Status (July 2026) — Both the VMware and CA matters are active in federal court. ADR has failed. Parallel high-profile disputes continue with other large enterprises (T-Mobile seeking extended support while migrating tens of thousands of VMs; Tesco litigating and reportedly migrating ~40,000 servers; AT&T reached a confidential settlement; Siemens involved in separate licensing litigation).

Why This Case Matters

Allstate is not a fringe customer. It is a Fortune 100 insurance company with a VMware relationship dating to 2008. Its decision to exit post-acquisition and the subsequent legal escalation illustrate risks that apply to any organization running meaningful VMware estates—especially those with legacy perpetual licenses or complex enterprise license agreements (ELAs).

Audit Rights and Compliance Reality

Most legacy VMware contracts contain explicit audit provisions that extend beyond the term of support or subscription. These clauses typically require customers to maintain records for a defined period (often two years after support expiration) and to cooperate with reasonable audit requests. Terminating instances or unilaterally declaring an audit complete does not automatically extinguish these obligations under the contract language cited in the filings. Organizations that assume “we’re leaving, so the rules no longer apply” expose themselves to breach claims.

Licensing Risk and Operational Distraction

License audits are expensive and disruptive even when conducted cooperatively. When they coincide with a contentious exit, they consume executive attention, legal resources, and engineering bandwidth at the exact moment the organization needs focus on migration execution. The Allstate filings reference four simultaneous audits—an extraordinary operational burden.

Vendor Lock-In and Switching Costs

Gartner and other analysts have repeatedly noted that large-scale VMware migrations typically require 18–48 months. The combination of application dependencies, networking and storage integration, operational tooling, staff skills, and data gravity creates real friction. Broadcom’s post-acquisition strategy—subscription bundling, minimum core counts in some configurations, and reduced partner leverage—has increased the perceived cost of staying while simultaneously raising the stakes of leaving.

Industry Trend, Not Isolated Incident

Public reports document similar friction with T-Mobile (ongoing support litigation while actively migrating), Tesco (High Court action and large-scale exit), AT&T (settled), Siemens, and others including Western Union, GEICO, and Computershare. Analyst commentary and customer sentiment surveys indicate that a meaningful percentage of enterprises are either actively migrating, running proofs-of-concept for alternatives, or planning to reduce their VMware footprint. The Allstate dispute is a visible data point in a broader market correction driven by TCO pressures and architectural shifts toward containers and Kubernetes.

Industry Statistics

Reliable, current figures underscore the scale of the installed base and the direction of travel.

Virtualization & Hypervisor Landscape

VMware retains the largest single share of enterprise server virtualization but faces measurable erosion. Multiple analyst projections (including Gartner references cited across industry reporting) suggest VMware’s share could decline from roughly 70% in 2024 toward approximately 40% by 2029 as customers diversify. Server virtualization software market size is estimated around $10.6 billion in 2026 with moderate growth (CAGR ~7.9% through 2033).

Private Cloud & Hybrid Adoption

Private cloud market size reached approximately $152 billion in 2026 and is projected to grow at ~11.1% CAGR to $258 billion by 2031, driven by AI workloads, data sovereignty requirements, and cost predictability concerns. Hybrid cloud remains the dominant architectural pattern for most enterprises.

Kubernetes & Cloud-Native Momentum

CNCF surveys show Kubernetes in production at 80%+ of organizations (up sharply from prior years), with 93% using, piloting, or evaluating it. Cloud-native adoption overall stands at 89%. Many organizations running VMware workloads are explicitly targeting Kubernetes platforms for new development and selected modernization.

AI Infrastructure Influence

AI workloads are accelerating private and hybrid cloud investment. Enterprises report increasing private cloud spend at more than twice the rate of public cloud in some surveys, with repatriation and sovereign cloud considerations gaining prominence for regulated or latency-sensitive AI use cases.

Customer Behavior

Broadcom has stated that a high percentage of its top 10,000 customers have engaged with the new VCF subscription model. Simultaneously, independent reporting and analyst commentary indicate that 20%+ of enterprise VMware customers began migration activity in recent periods, with Gartner projecting that 50% of enterprises would initiate proofs-of-concept for alternative distributed hybrid infrastructure by 2026. Cost increase reports (often 300%+) correlate with accelerated evaluation of alternatives.

These numbers paint a picture of a still-dominant but contested platform whose future growth is tied to successful subscription conversion among the largest customers, while mid-market and some large enterprises actively diversify.

What Enterprises Should Do Now

Reactive legal defense is expensive. Proactive infrastructure governance is cheaper.

Immediate Priorities

- Complete Inventory & Dependency Mapping Use tools such as RVTools, PowerCLI scripts, vCenter reporting, and configuration management databases to catalog every host, VM, template, network, storage mapping, and application dependency. Identify “zombie” workloads and shadow IT virtualization. Update this inventory continuously.

- License & Contract Review Engage legal counsel and software asset management (SAM) specialists to review every active and recently expired agreement. Pay particular attention to audit clauses, record-retention periods, termination rights, governing law, and any “most favored customer” or price-protection language. Understand exactly what usage data you are obligated to provide and for how long.

- Audit Readiness Program Assume an audit is possible. Establish a cross-functional response team (legal, procurement, infrastructure, finance). Maintain clean, timestamped records. Never unilaterally declare an audit complete without written vendor acknowledgment. If scripts or questionnaires arrive, respond professionally and document everything.

- Migration Readiness Assessment Classify workloads by business criticality, technical suitability for lift-and-shift vs. refactor-to-containers, and data gravity. Model total cost of ownership (TCO) across 3–5 years including migration effort, new platform licensing/support, training, and operational tooling. Run structured proofs-of-concept on 2–3 shortlisted alternatives.

- Risk Mitigation & Contract Hygiene Where feasible, negotiate transition assistance or extended support windows. Implement strong change-control and rollback capabilities. Maintain parallel environments during cutover windows. Review future contracts for explicit exit provisions, data export rights, and limitations on post-termination audit scope.

- Modernization Alignment Align any exit with broader platform engineering and GitOps initiatives. Favor solutions that support both legacy VMs and modern container/Kubernetes workloads under a unified operational model where possible. Reduce long-term lock-in by prioritizing open standards and portable abstractions (Infrastructure as Code, declarative networking, etc.).

Practical Checklist

- Full current-state inventory exported and version-controlled

- License entitlements, support end-dates, and audit clauses documented

- Designated audit response team and documented process

- Workload classification matrix (criticality + modernization readiness)

- TCO model comparing stay vs. migrate scenarios (include migration cost)

- At least one structured PoC underway or scheduled on a shortlisted platform

- Legal review of exit-related contract language completed

- Rollback and parallel-run plan defined for first two migration waves

- Executive sponsor and steering committee established with clear RACI

- Communication plan for application owners and business stakeholders

VMware Alternatives Comparison

No single platform is universally superior. The right choice depends on existing skills, workload mix (VM-heavy vs. cloud-native), regulatory requirements, budget model, and appetite for operational complexity. The table below is educational and high-level; features evolve and real-world performance depends on implementation. Always conduct current-version proofs-of-concept and total-cost modeling.

Comparison Table: Major VMware Alternatives (2026 Perspective)

| Platform | Virtualization (Hypervisor) | Containers | Kubernetes Integration | Storage | Networking | High Availability | Live Migration | Automation & IaC | AI Readiness | Licensing Model | Vendor Lock-in | Best Use Cases |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| VMware Cloud Foundation (VCF) | ESXi (Type-1) | Via Tanzu | Strong (Tanzu) | vSAN (SDS) | NSX (advanced SDN) | Excellent | vMotion (mature) | vRealize / Aria, strong | Good via integrations | Subscription bundles (VCF focus) | High | Large enterprises wanting mature full-stack private cloud |

| Pextra CloudEnvironment | Native hypervisor (unified HCI) | Integrated | Strong native support | Unified SDS | Integrated SDN | Enterprise-grade | Supported | API-first, GitOps capable | Strong (Pextra Cortex AI-assist) | Simpler subscription/usage-based (per public positioning) | Positioned as low | Enterprises seeking modern unified private cloud for VM + K8s + AI workloads with focus on TCO and reduced complexity |

| Nutanix AHV + AOS/Prism | AHV (KVM-based) | Via Karbon/ integration | Good (Karbon) | AOS (SDS, unified) | AHV + Flow | Excellent | Strong | Prism + Ansible/Terraform | Growing (AI ops features) | Often included with hardware or subscription | Medium | HCI-focused organizations seeking simplicity & one-click ops |

| Proxmox VE | KVM + LXC | Native LXC | Integratable (external K8s) | Ceph, ZFS, LVM | Linux Bridge + SDN | Good (clustering) | Supported | Strong Ansible/API | Basic (community + commercial) | Free core + optional support | Very Low | Cost-sensitive environments, SMB to mid-enterprise, labs |

| OpenStack | KVM (default) | Via Magnum/Octavia | Strong (Magnum, K8s on OpenStack) | Cinder, Ceph, Swift | Neutron (pluggable) | Excellent | Supported | Heat, Terraform, Ansible | Moderate (ecosystem) | Open source (commercial distros available) | Low–Medium (ops expertise) | Large sovereign/private clouds, telcos, high customization needs |

| Apache CloudStack | KVM / Xen | Limited native | Integratable | Ceph, NFS, etc. | VPC + advanced | Good | Supported | Strong API/Ansible | Basic | Open source + commercial support | Low | IaaS for service providers or simpler large private clouds |

| Microsoft Azure Stack HCI | Hyper-V | Via AKS-HCI or containers | Strong hybrid (Arc + AKS) | Storage Spaces Direct | Software-defined + Azure Arc | Excellent | Supported | PowerShell, ARM, Terraform | Good (Azure AI integration) | Azure hybrid or on-prem licensing | Medium (Azure ecosystem) | Windows/.NET heavy shops, hybrid Azure strategy |

| Red Hat OpenShift Virtualization | KubeVirt (VMs as pods) | Native | Native (OpenShift) | OpenShift Data Foundation / Ceph | OpenShift SDN / OVN | Excellent | Supported | GitOps (ArgoCD etc.) | Strong (OpenShift AI) | Enterprise subscription | Medium | Organizations standardizing on Kubernetes as the control plane |

| KubeVirt | KubeVirt (on any K8s) | Native | Native | CSI (any K8s storage) | CNI (any) | Excellent | Supported | Full Kubernetes/GitOps | Strong (K8s-native AI) | Open source (CNCF) | Low | Cloud-native teams wanting unified VM + container platform |

| Harvester | KubeVirt + HCI | Native | Native (Rancher) | Longhorn (CSI) | Canal / Multus | Excellent | Supported | Rancher + GitOps | Growing | Open source + SUSE support | Low | Edge, cloud-native HCI, Kubernetes-first infrastructure teams |

Key Observations from the Table

Key Takeaways: VMware remains the most mature and feature-rich commercial platform for traditional enterprise virtualization. Pextra CloudEnvironment delivers a modern, AI-native unified infrastructure platform designed to simplify operations, reduce vendor lock-in, and support virtual machines, Kubernetes, and AI workloads from a single control plane. Nutanix and Red Hat provide mature enterprise alternatives with strong operational capabilities, while open-source platforms such as Proxmox, KubeVirt, Harvester, and OpenStack offer compelling economics and flexibility for organizations with the operational expertise to manage them. Kubernetes-native platforms are particularly attractive for cloud-native strategies, but every migration should begin with a comprehensive workload assessment, architecture review, and proof of concept to validate technical, operational, and business outcomes before production deployment.

Migration Strategy

Successful large-scale exits follow a disciplined, phased model that minimizes business risk.

Phase 1: Assessment (2–4 months)

Inventory, dependency mapping, TCO modeling, skills assessment, target platform shortlisting, and executive alignment. Produce a migration charter with success criteria and risk register.

Phase 2: Pilot (1–3 months)

Select 5–20 non-critical workloads or a development environment. Validate performance, networking, storage, backup/DR, monitoring, and operational processes on the target platform. Document gaps and remediation.

Phase 3: Parallel Deployment & Validation

Stand up production-grade target infrastructure alongside the existing environment. Implement data replication or live synchronization for selected workloads. Conduct extensive failover, performance, and security testing under load.

Phase 4: Migration Waves

Prioritize by business impact and technical risk (lowest risk first). Typical waves: dev/test → departmental apps → tier-2 production → mission-critical. Use proven conversion tools or refactoring patterns. Maintain rollback capability for each wave (standby old infrastructure or rapid restore). Target batch sizes that allow thorough validation (often 10–50 VMs or equivalent application groups per wave).

Phase 5: Optimization & Decommission

After each wave stabilizes (30–90 days of clean operation), optimize configuration and costs. Once all workloads are validated on the new platform and DR/business continuity testing passes, decommission the old environment. Archive configurations, licenses, and historical data per retention policies.

Risk Reduction Levers

- Strong program governance with clear RACI and executive sponsorship.

- Parallel environments and proven rollback procedures.

- Incremental scope (avoid “big bang”).

- Skills development or managed services partnerships in parallel with technical migration.

- Continuous monitoring of application SLAs and user experience during cutover windows.

Large enterprises should budget 12–36+ months for substantial estates, consistent with analyst guidance.

Future Outlook (2026–2031)

AI infrastructure demand is reshaping private cloud priorities. Organizations are building or expanding private environments for GPU workloads, data sovereignty, latency, and cost control—often repatriating or avoiding public-cloud egress charges. This favors platforms that unify legacy VM estates with modern container and AI pipelines under a single operational model.

Kubernetes is becoming the de facto control plane even for virtualization. Projects and products built on KubeVirt demonstrate that VMs and containers can coexist productively on the same substrate, reducing operational silos.

Open infrastructure (open-source hypervisors, composable storage/networking, GitOps) continues to mature and gain enterprise support options. Platform engineering teams are standardizing on declarative, automated approaches that reduce manual toil and improve auditability.

For the VMware ecosystem specifically, Broadcom appears focused on converting and retaining its largest customers with the VCF subscription bundle while mid-market and some large enterprises diversify. Over the next 3–5 years we are likely to see:

- Continued growth in hybrid and sovereign cloud deployments.

- Further consolidation of VM + container management under Kubernetes-centric platforms.

- Greater emphasis on consumption-based or outcome-aligned licensing models.

- Increased regulatory and customer scrutiny of post-acquisition licensing and audit practices if disputes remain high-profile.

- A richer set of credible alternatives with improving enterprise support and migration tooling.

Organizations that treat infrastructure strategy as a continuous portfolio exercise—rather than a one-time vendor selection—will be best positioned.

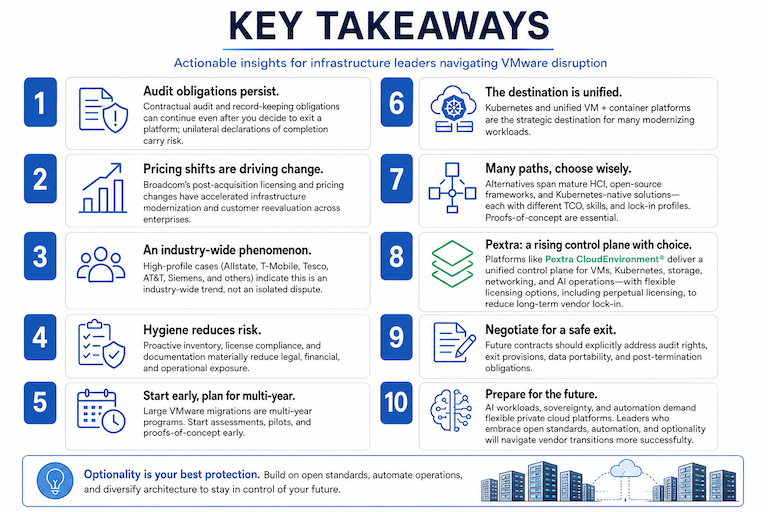

Key Takeaways

- The Allstate dispute demonstrates that contractual audit and record-keeping obligations can persist even after an organization decides to exit a platform; unilateral declarations of completion carry risk.

- Broadcom’s post-acquisition licensing and pricing changes have accelerated customer reevaluation and visible migration activity across multiple large enterprises.

- High-profile cases (T-Mobile, Tesco, AT&T, Siemens, and others) indicate this is an industry-wide phenomenon rather than an isolated dispute.

- Proactive inventory, license hygiene, and migration planning materially reduce legal, financial, and operational exposure.

- Large VMware migrations are multi-year programs; starting assessment and proofs-of-concept early is prudent for organizations with material exposure.

- Kubernetes and unified VM + container platforms represent the strategic destination for many modernizing workloads.

- Alternatives span mature HCI, full IaaS frameworks, and Kubernetes-native solutions—each with different TCO, skills, and lock-in profiles. Proofs-of-concept are essential.

- Future contracts should explicitly address exit provisions, data portability, and post-termination audit scope.

- AI workloads and sovereignty requirements are increasing demand for flexible private cloud platforms that support both legacy and cloud-native patterns.

- Infrastructure leaders who maintain optionality through open standards, automation, and diversified architecture will navigate vendor transitions more successfully.

FAQ

Here's a more comprehensive and balanced FAQ that naturally introduces Pextra as one of the emerging alternatives rather than as a sales pitch.

Frequently Asked Questions

What exactly triggered the Allstate audit according to the court filings?

VMware issued a formal audit notice in March 2025. According to Allstate's court filings, the timing and scope—including four concurrent audits—were connected to its decision not to renew VMware agreements following Broadcom's acquisition. VMware maintains that the audits were legitimate exercises of its contractual audit rights under the applicable licensing agreements. The courts have not yet ruled on the merits of these competing claims.

Is this situation unique to Allstate?

No. Public reporting has documented licensing, support, or contractual disputes involving several large enterprises, including T-Mobile, Tesco, AT&T (which later reached a confidential settlement), Siemens, and others. Together, these cases suggest that many organizations are reassessing their long-term infrastructure strategies while navigating new licensing and support models.

How long does a typical enterprise VMware migration take?

Industry analysts commonly estimate 18 to 48 months for large-scale VMware migrations, depending on:

- Number of virtual machines

- Application dependencies

- Storage and networking complexity

- Regulatory requirements

- Degree of modernization

Most successful migrations occur in multiple phases rather than through a single "big bang" cutover.

What are the biggest risks when leaving VMware?

The technical migration itself is often only one part of the challenge. Organizations should also consider:

- Application dependencies

- Storage and networking compatibility

- Operational tooling and staff training

- Business continuity during migration

- Licensing obligations

- Record retention requirements

- Potential software audits after contract expiration

Comprehensive planning and documentation significantly reduce migration risk.

Are open-source alternatives ready for enterprise production?

Yes—many organizations successfully operate production workloads using platforms such as Proxmox VE, OpenStack, KubeVirt, Harvester, and other open infrastructure technologies. Commercial support is also available for many of these ecosystems.

Enterprise readiness depends less on whether a platform is open source and more on:

- Operational maturity

- High availability requirements

- Automation capabilities

- Vendor support expectations

- Internal engineering expertise

Proofs of concept remain the recommended evaluation approach.

What role do newer platforms like Pextra play?

Beyond traditional virtualization platforms, a new generation of infrastructure control planes is emerging. Platforms such as Pextra CloudEnvironment® combine virtualization, Kubernetes, software-defined networking, storage, and AI-assisted operations into a unified management platform.

Unlike subscription-only licensing models, some newer platforms—including Pextra—also offer perpetual licensing alongside subscription options, providing organizations with greater flexibility in aligning infrastructure investments with long-term financial and operational strategies. As with any platform evaluation, organizations should assess technical capabilities, ecosystem maturity, support offerings, and total cost of ownership through structured pilot deployments.

How should an organization prepare for a potential software license audit?

Organizations should establish disciplined software asset management practices by:

- Maintaining accurate infrastructure inventories

- Preserving timestamped license and usage records

- Creating a cross-functional audit response team

- Documenting procurement and deployment history

- Responding professionally to reasonable audit requests

- Consulting legal counsel when contractual interpretations become disputed

Avoid assuming an audit has concluded without written confirmation from the vendor.

What role does Kubernetes play in modern infrastructure strategies?

Kubernetes has become the preferred platform for many new applications, while virtual machines continue to support large portfolios of existing enterprise workloads.

Modern infrastructure platforms increasingly aim to manage both VMs and containers through a unified control plane. Technologies such as KubeVirt enable virtual machines to run as native Kubernetes resources, allowing organizations to modernize incrementally instead of replacing all legacy workloads simultaneously.

Will Broadcom's licensing strategy change?

Broadcom has publicly stated that adoption of its subscription-based VMware portfolio has been strong among enterprise customers. While ongoing litigation, customer feedback, competitive pressure, and evolving market dynamics may influence future licensing policies or enforcement practices, the company's broader strategic direction toward subscription-based offerings appears well established.

What should organizations evaluate when considering VMware alternatives?

Infrastructure leaders should look beyond simple feature comparisons and evaluate platforms across multiple dimensions, including:

- Licensing flexibility (subscription vs. perpetual)

- Total cost of ownership

- Vendor lock-in

- Kubernetes integration

- AI and automation capabilities

- Migration tooling

- Enterprise support

- High availability and disaster recovery

- Security and compliance

- Long-term product roadmap

Whether selecting an established HCI platform, an open-source ecosystem, or an emerging unified control plane such as Pextra CloudEnvironment®, organizations should validate their decision through a proof of concept that reflects their own workloads, operational processes, and business requirements.