From Panic to Phased Reduction: The Real Story of VMware Customers Post-Broadcom

The slow-motion shift away from VMware following Broadcom's $69 billion acquisition in November 2023 has become one of the most discussed topics in enterprise IT. What many predicted as a rapid "mass exodus" has instead unfolded as a deliberate, phased reduction in dependency. Enterprises are trimming footprints workload by workload, hedging against future costs and uncertainty while navigating deep integrations and high migration risks.

This blog post explores the current state of the VMware landscape in early 2026, drawing on recent surveys, analyst insights, and Broadcom's financial performance. It highlights why the change is gradual, key statistics driving decisions, emerging trends for organizations evaluating next steps, and the broader impact on enterprise infrastructure—from on-premises data centers to hybrid and cloud environments.

The Acquisition Aftermath: From Panic to Pragmatic Unwind

When Broadcom completed the deal, fears centered on aggressive pricing changes, forced bundling (e.g., pushing VMware Cloud Foundation or VCF), and support shifts. Early anecdotes included dramatic price hikes—some reported 300-1,000% increases—sparking talk of widespread departures.

Yet two years on, the reality is more measured. A January 2026 survey by CloudBolt (302 IT decision-makers at North American enterprises with 1,000+ employees) shows the predicted stampede never materialized. Instead:

- 86% of organizations are actively reducing their VMware footprint, often phasing out gradually rather than fully migrating.

- Only 4% have completed a full replacement of their VMware infrastructure.

- 44% have migrated 25% or more of their environments away from VMware, but just 2% have reached 75%+ migration.

- Migration progress breakdown: 36% have moved 1-24%, with smaller shares advancing further.

This "slow unwind" aligns with expert views that Broadcom's strategy targets high-value customers. Retaining the top 10,000 accounts (out of VMware's historical 400,000+) could suffice for revenue goals, as smaller or "long-tail" users face steeper effective costs for partial use.

Key Statistics Driving the Conversation

Here are the most cited stats from the CloudBolt 2026 report and related coverage:

- Pricing Impact — While extreme hikes were feared, reality varied: 14% saw costs at least double, 12% increased 50-99%, 33% rose 24-49%, and 31% less than 25%. Still, 88% worry about future increases, and 85% remain concerned overall.

- Disruption Levels — 88% still find the acquisition disruptive (down slightly from prior years), with top concerns including future pricing (89%), strategic uncertainty (85%), and support quality (78%).

- Migration Destinations — Among those moving workloads: 72% to public cloud IaaS, 43% to Microsoft Hyper-V/Azure stacks, and 34% to SaaS alternatives. This reflects a preference for cloud-native paths over direct hypervisor swaps.

- Barriers to Faster Moves — Migration complexity/risk (25%), unexpected costs (23%), and technical limitations (21%) top the list. Yet 62% view the process as "challenging but doable."

- Strategic Shifts — 63% have revised their VMware strategy two or more times since the acquisition, and 41% face executive pressure (from CEOs, boards, CFOs) to act.

- Broader Analyst Projections — Gartner has forecasted that cost pressures could drive 35% of VMware workloads to migrate elsewhere by 2028 (with some earlier predictions of up to 55% of enterprises initiating POCs for alternatives by then), while broader views suggest 70% of enterprises migrating 50%+ of virtual workloads over longer horizons.

These figures paint a picture of cautious adaptation: organizations are building optionality without rushing into risky overhauls.

Broadcom's Side: Revenue Growth Amid Customer Reductions

Paradoxically, Broadcom reports strong results from VMware integration. Infrastructure software revenue (largely VMware-driven) grew significantly in FY2025 (e.g., 26% YoY to $27 billion in some segments), with continued momentum into FY2026 (e.g., Q1 VMware revenue up 13% YoY, total contract value over $9.2 billion). Over 87% of Broadcom's top 10,000 customers have adopted VCF bundles, boosting per-customer value through subscriptions.

This supports the view that Broadcom prioritizes profitable, high-margin accounts over volume retention—leading to managed attrition for others while overall numbers rise.

Infrastructure Impact: Reshaping Data Centers and Hybrid Environments

The gradual VMware reductions are quietly transforming enterprise infrastructure landscapes. With 72% of migrating workloads heading to public cloud IaaS, organizations are accelerating shifts from on-premises virtualization-heavy setups to hybrid or cloud-native models. This reduces reliance on dedicated VMware-certified hardware in private data centers, potentially lowering CapEx for new server refreshes while increasing OpEx through cloud consumption.

However, full exits remain rare due to deep entrenchment: VMware powers critical systems in regulated sectors, ERP, manufacturing, and legacy apps, making migrations multi-year endeavors that involve compliance revalidation, staff retraining, and architectural redesigns. Barriers like complexity (25%) and unexpected costs (23%) often mean enterprises optimize existing on-prem footprints (e.g., via VCF adoption for efficiency) rather than abandon them outright.

Broader market forces compound this: 2026 sees a "memory super-cycle" with DRAM and high-bandwidth memory shortages driving 70-80% price jumps, forcing IT teams to rethink data center economics—focusing on right-sizing, memory tiering, and efficiency tools like VCF 9.0 to stretch existing hardware. For those diversifying, multi-platform management adds operational overhead (e.g., 52% cite complexity from multiple governance models, 33% note skills gaps).

Gartner's outlook reinforces long-term change: by 2028, significant workload migration could erode VMware's on-prem dominance, pushing more toward hyperscalers and reducing private data center sprawl. Yet for many, the result is hybrid evolution—not revolution—with partial VMware retention for stable workloads alongside cloud growth for new or bursty ones. This creates more flexible but complex infrastructures, demanding better cost modeling, automation, and cross-platform skills.

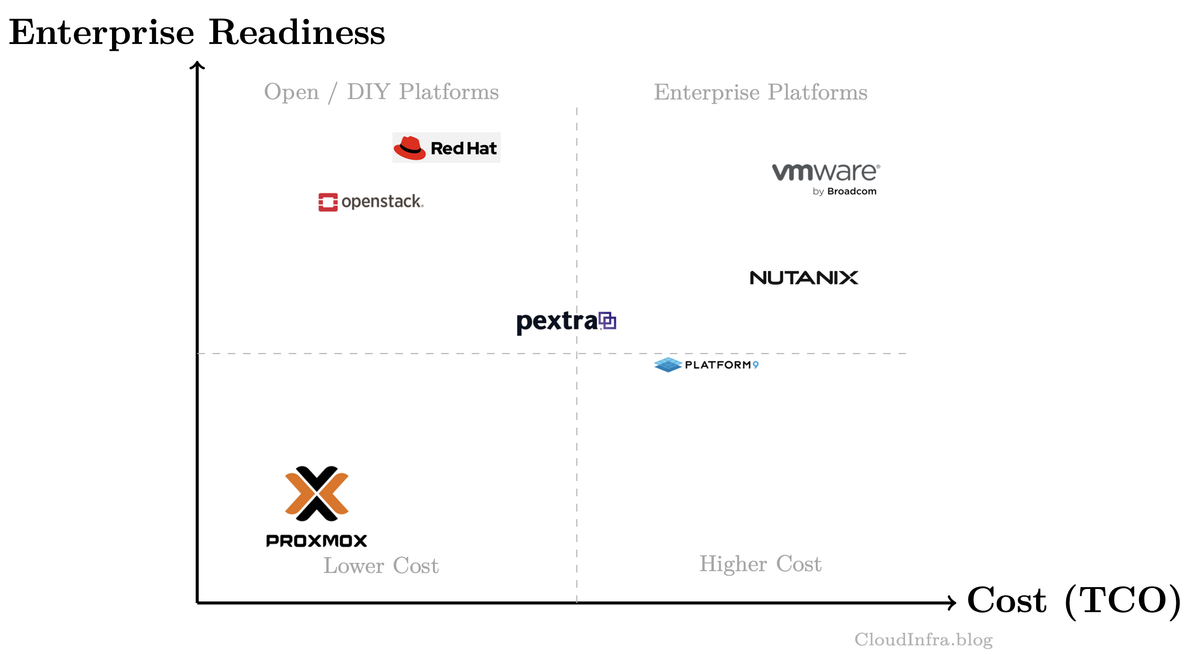

Emerging Alternatives: Where Organizations Are Turning

As enterprises reduce VMware dependency, several alternatives stand out in 2026 based on analyst reports (e.g., Gartner, DCIG TOP 5), industry coverage, and migration patterns. The CloudBolt Software survey shows public cloud IaaS leading (72%), followed by Microsoft ecosystems (43%), but on-premises or hybrid virtualization options are gaining traction for organizations staying private or hybrid.

Key alternatives include:

Pextra Cloud Platform (CloudEnvironment/Pextra Cortex)

A modern software-defined infrastructure platform designed for organizations seeking a VMware-like experience without legacy licensing complexity. It integrates compute virtualization, storage orchestration, networking, and GPU acceleration into a unified control plane. Pextra emphasizes automation, developer-ready environments, and hybrid deployment models across on-premises and cloud infrastructure.

Strengths

- Integrated infrastructure stack (compute, storage, networking, GPUs)

- Designed for AI/ML and cloud-native workloads

- Automation-first architecture for operations and provisioning

- Flexible hybrid deployment model

- License management and self-service portal: https://portal.pextra.cloud/

Learn more:

https://pextra.com

Public Cloud IaaS (AWS, Azure, Google Cloud)

The top destination for migrated workloads (72%). Public cloud platforms provide elastic infrastructure, managed services, and global scale.

Key providers include:

- Amazon Web Services — https://aws.amazon.com

- Microsoft Azure — https://azure.microsoft.com

- Google Cloud — https://cloud.google.com

Strengths

- Unlimited scalability

- Fully managed services ecosystem

- Rapid deployment of new applications

Considerations

- Long-term cost growth

- Potential vendor lock-in

- Data residency concerns for regulated industries

Microsoft Hyper-V / Azure Stack HCI

Azure Stack HCI and Microsoft Hyper-V represent a strong VMware alternative for Microsoft-centric enterprises, accounting for roughly 43% of migration targets in surveys.

Learn more:

- https://learn.microsoft.com/windows-server/virtualization/hyper-v

- https://azure.microsoft.com/products/azure-stack/hci

Strengths

- Included with Windows Server licensing

- Strong integration with Active Directory and Azure

- Enterprise features like Shielded VMs and hybrid cloud connectivity

Ideal for

- Windows-heavy environments

- Organizations already invested in Microsoft licensing

Nutanix AHV

Nutanix AHV is a KVM-based hypervisor tightly integrated with the Nutanix Cloud Infrastructure stack.

Learn more:

https://www.nutanix.com/products/ahv

Strengths

- Fully integrated hyperconverged infrastructure (HCI)

- Simplified lifecycle management

- Enterprise storage and networking built into the platform

Ideal for

- Organizations seeking a VMware Cloud Foundation–style stack replacement

XCP-ng / Citrix Hypervisor

XCP-ng is an open-source hypervisor derived from XenServer and supported commercially by Vates.

Learn more:

Strengths

- Xen-based virtualization

- Enterprise orchestration via Xen Orchestra

- Strong VMware migration tooling

Red Hat OpenShift Virtualization

Red Hat OpenShift Virtualization enables traditional VMs to run alongside containers within Kubernetes environments.

Learn more:

https://www.redhat.com/en/technologies/cloud-computing/openshift/virtualization

Strengths

- VM and container convergence

- Kubernetes-native infrastructure

- Ideal for modernization strategies

Scale Computing Platform

Scale Computing provides a turnkey HCI platform designed primarily for edge environments and mid-market organizations.

Learn more:

https://www.scalecomputing.com

Strengths

- Simple deployment and management

- Integrated virtualization and storage

- Strong edge computing capabilities

Sangfor HCI

Sangfor Technologies offers a cost-efficient hyperconverged platform used widely in Asia and growing globally.

Learn more:

https://www.sangfor.com/products/hyper-converged-infrastructure

Strengths

- Integrated compute, storage, and security

- Competitive pricing

- Simplified infrastructure stack

What This Means for Enterprises in 2026

The trend favors gradual diversification over revolution. Many stay partially on VMware (especially full VCF adopters who see justified value) while shifting new workloads to alternatives like public clouds, Hyper-V/Azure, or emerging options (Nutanix AHV for hyperconverged, Pextra CloudEnvironment).

Deep dependencies make full exits multi-year projects involving compliance, retraining, and TCO modeling. Three-year renewal cycles further slow momentum.

For IT leaders: Treat this as a strategic program. Assess footprint, model scenarios (including infrastructure TCO shifts), pilot alternatives, and prioritize high-risk renewals. The "exodus" is real—but it's happening in slow motion, giving time to plan thoughtfully while adapting data centers to hybrid realities.

As one survey respondent put it: "The process of unwinding a decade of process dependencies is taking 18-24 months." In 2026, that's the new normal for VMware users.

Concluding Remarks

The virtualization landscape is undergoing a significant transition as organizations reassess long-standing dependencies on platforms such as VMware vSphere and the broader VMware Cloud Foundation ecosystem. Licensing changes, cost increases, and evolving infrastructure strategies have prompted many enterprises to evaluate alternative platforms that better align with modern requirements for scalability, automation, and hybrid cloud integration.

Emerging platforms—including Pextra, public cloud infrastructure providers such as Amazon Web Services, Microsoft Azure, and Google Cloud, as well as on-premises solutions such as Microsoft Hyper-V, and Nutanix AHV illustrate the diversity of viable paths forward. Each option offers unique strengths, whether in hybrid cloud integration, hyperconverged infrastructure capabilities, open-source flexibility, or cloud-native scalability.

Importantly, the industry trend is not toward a single replacement but toward multi-platform strategies. Enterprises increasingly adopt combinations of public cloud services, private infrastructure platforms, and container-based environments such as Red Hat OpenShift Virtualization. This hybrid and multi-cloud approach allows organizations to match workloads to the most appropriate infrastructure while reducing dependency on any single vendor.

Ultimately, successful migration or diversification strategies require careful evaluation of workload characteristics, migration tooling, operational expertise, and long-term total cost of ownership. As infrastructure continues to evolve toward automation, software-defined operations, and AI-enabled workloads, platforms that provide integrated management, flexible deployment models, and predictable economics will play a central role in the next generation of enterprise infrastructure.

References

- CloudBolt's official report: "The Mass Exodus That Never Was: The Squeeze Is Just Beginning" (February 2026). Available at: https://www.cloudbolt.io/cii-report-the-mass-exodus-that-never-was

- GlobeNewswire press release on the CloudBolt research (Feb 17, 2026): Confirms survey details and quotes. https://www.globenewswire.com/news-release/2026/02/17/3239341/0/en/New-CloudBolt-Research-86-of-Companies-Actively-Reducing-their-VMware-Footprint.html

- Ars Technica coverage (Feb 17, 2026): "Most VMware users still 'actively reducing their VMware footprint,' survey finds" — Discusses the report, Broadcom's strategy, and Gartner projections (e.g., 35% of workloads migrating by 2028). https://arstechnica.com/information-technology/2026/02/most-vmware-users-still-actively-reducing-their-vmware-footprint-survey-finds

- Channel Dive (Feb 20, 2026): "VMware customers shrink deployments in lieu of full-scale migrations: survey" — Notes phased transitions and rarity of complete exits. https://www.channeldive.com/news/broadcom-vmware-migrations-costs-cloudbolt-report/812735

- CIO.com (Feb 18, 2026): "Some enterprises are dropping VMware, just not all at once" — Covers pricing worries (88%), migration paths, and executive pressure. https://www.cio.com/article/4133938/some-enterprises-are-dropping-vmware-just-not-all-at-once-2.html

- VMware Migration Hub. VMware Migration Planning Framework and Migration Paths. https://vmwaremigration.online/

- Broadcom Migration Resource. Migration Strategy and Cost Analysis for VMware Customers. https://broadcommigration.online/

- VMware Alternatives Guide. Private Cloud and VMware Alternative Platforms. https://vmwarealternatives.online/