The AI Reckoning: Why Cloud Infrastructure Must Be Rewritten for the Intelligence Era

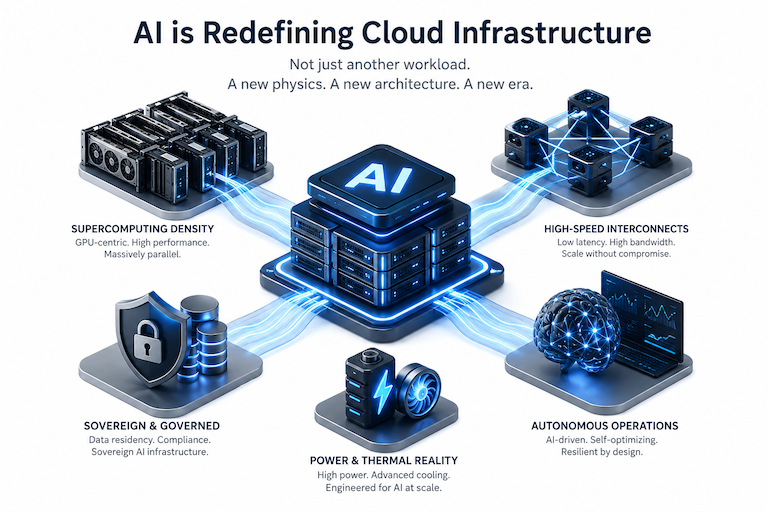

Enterprise architects and infrastructure leaders have long treated the cloud as an elastic, abstracted layer of general-purpose compute, networking, and storage. That model, optimized for web-scale applications, databases, and virtual machines, is colliding with a fundamentally different class of workload. Artificial intelligence, particularly large language models, agentic systems, and distributed inference, does not merely run on infrastructure. It dictates its physics, density, interconnects, power profile, governance, and even its geography.

This is not incremental evolution. It is a structural break. Over the next decade, the organizations that succeed will treat AI infrastructure as a distinct engineering discipline: part supercomputing, part distributed systems, part sovereign asset, and increasingly, part autonomous operations platform.

Executive Summary

AI workloads differ from traditional enterprise applications in nearly every dimension: they are accelerator-centric rather than CPU-centric; they demand extreme memory bandwidth, low-latency scale-up fabrics (NVLink domains acting as single logical GPUs), and gang-scheduled distributed execution; they are sensitive to data locality and power/thermal constraints at rack scales previously unimaginable (120–140+ kW per rack for current-generation systems); and they introduce new requirements for sovereignty, model protection, and cost predictability that public cloud economics often fail to satisfy at production scale.

Traditional stacks—VMware-centric virtualization, SANs, classic three-tier designs, and even early hyperconverged infrastructure—face real pressure but are not obsolete. Evidence from 2026 shows production AI inference shifting decisively toward private cloud environments for cost, control, security, and compliance reasons. VMware Cloud Foundation and similar platforms are being repositioned precisely for this mixed VM/container/AI accelerator world.

AI-native patterns are emerging rapidly: GPU pools with advanced scheduling (Kubernetes enhancements for gang scheduling, Dynamic Resource Allocation, topology awareness, and fractional sharing via MIG/time-slicing); rack-scale composable systems; DPUs for offload; and early AI-managed operations (predictive healing, intent-driven placement, AIOps). Hardware is iterating at unprecedented speed—NVIDIA Blackwell GB200 NVL72 racks already deliver 30× real-time LLM inference versus prior generations in liquid-cooled designs, with Vera Rubin platforms (announced GTC 2026) targeting further leaps in inference efficiency and agentic workloads.

Sovereign and private AI infrastructure is accelerating as governments and regulated enterprises prioritize data residency, national security, and independence from hyperscaler concentration. Power and cooling have become first-order constraints, driving liquid cooling adoption and on-site generation strategies. Economics favor high utilization and private deployments for sustained workloads, even as capex remains enormous.

By 2027–2030, expect hybrid architectures (private AI factories + public burst + sovereign cores) to dominate, with Kubernetes maturing as the orchestration layer for AI workloads alongside (not fully replacing) evolved virtualization. By 2035, infrastructure may look more like autonomous “intelligence manufacturing platforms” than today’s abstracted cloud—self-optimizing, policy-driven, and geographically bounded by sovereignty requirements. NVIDIA’s full-stack ecosystem, Broadcom/VMware’s enterprise private cloud positioning, open-source Kubernetes operators, and hyperscalers with sovereign offerings are best positioned, but success will hinge on skills blending traditional infrastructure depth with AI-specific scheduling, power/thermal engineering, and autonomous operations.

Why AI Workloads Break Traditional Assumptions

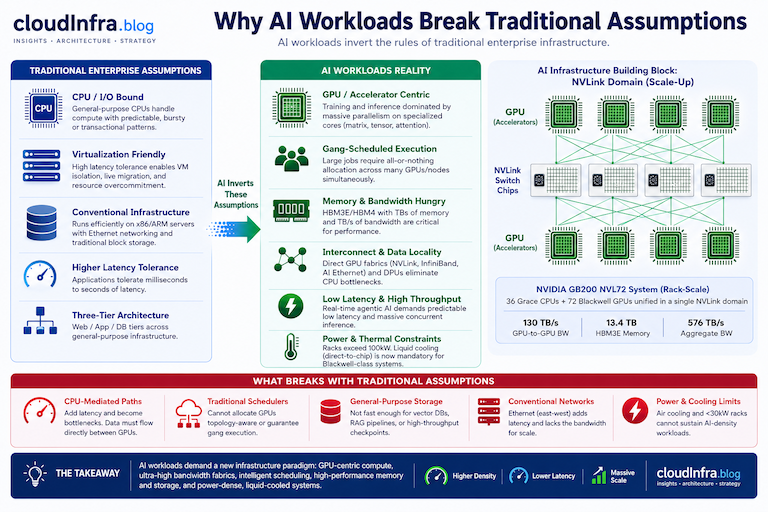

Traditional enterprise applications are typically CPU-bound or I/O-bound, with relatively predictable, bursty, or transactional patterns. They tolerate higher latency, benefit from virtualization’s isolation and live migration, and run efficiently on general-purpose x86/ARM servers with conventional Ethernet and block storage.

AI workloads invert this:

- GPU/accelerator-centric computing: Training and inference are dominated by matrix operations on thousands of specialized cores. A single GB200 Grace Blackwell Superchip pairs one Grace CPU with two Blackwell GPUs via NVLink-C2C; a full GB200 NVL72 rack-scale system unifies 36 Grace CPUs and 72 Blackwell GPUs into what NVIDIA describes as the largest NVLink domain ever, effectively acting as a single massive GPU with 130 TB/s GPU-to-GPU bandwidth.

- Distributed and gang-scheduled execution: Large training jobs or coordinated inference require simultaneous allocation across many GPUs/nodes (“all-or-nothing”). Traditional schedulers fail here; new Kubernetes features (Workload Aware Scheduling, PodGroup, Kueue, NVIDIA KAI Scheduler) address gang semantics and topology awareness.

- Memory bandwidth and capacity hunger: HBM3E/HBM4 dominates. GB200 NVL72 provides 13.4 TB HBM3E GPU memory at 576 TB/s aggregate bandwidth. Future Rubin platforms push this dramatically higher.

- Interconnect and data locality: CPU-mediated data movement kills performance. Direct GPU fabrics (NVLink scale-up, InfiniBand or AI-optimized Ethernet scale-out) and DPUs (BlueField) for offload are essential. Vector databases and RAG pipelines add storage throughput and low-latency retrieval demands.

- Latency and agentic requirements: Real-time agentic AI (multi-step reasoning, tool use, long context) demands predictable low latency and high throughput inference, not just batch training. Power density and thermal limits become hard constraints—racks routinely exceed 100 kW, with liquid cooling (direct-to-chip) now mandatory for Blackwell-class systems rather than optional.

These characteristics make classic three-tier designs, general-purpose hypervisors without GPU awareness, and purely CPU-orchestrated clouds inefficient or outright unsuitable for frontier workloads.

Is the Traditional Enterprise Infrastructure Stack Becoming Obsolete?

No—but it must evolve. The role of the traditional enterprise stack is being redefined.

Virtualization, private cloud, and infrastructure platforms remain highly relevant; however, the requirements of the AI era are exposing limitations in architectures designed primarily for general-purpose workloads.

The market is shifting from virtualization-centric infrastructure toward AI-optimized, sovereign, and intelligent infrastructure control planes.

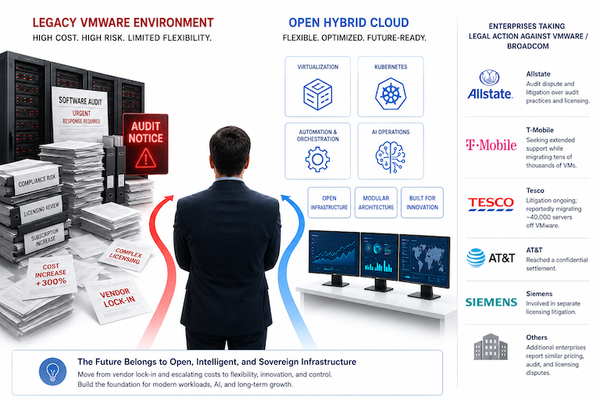

Broadcom’s Private Cloud Outlook 2026 survey of 1,800 senior IT leaders highlights this transition: production AI inferencing is increasingly moving toward private cloud environments, with 56% of organizations running or planning to run AI inference privately versus 41% in public cloud. Workload repatriation is accelerating, with cost predictability, security, governance, and sovereignty becoming primary drivers. Cost has now overtaken security as the leading public-cloud concern.

This does not represent a rejection of cloud—it represents a maturation of enterprise infrastructure strategy.

VMware: Strong Foundation, New Strategic Position

VMware remains one of the most widely deployed enterprise virtualization platforms. The evolution toward VMware Cloud Foundation reflects the industry shift toward unified environments that manage:

- Virtual machines and containers

- Kubernetes workloads

- AI accelerators and GPU resources

- Security, governance, and lifecycle management

VMware’s direction demonstrates that enterprise virtualization is not disappearing; it is becoming a foundation layer for private AI infrastructure.

However, Broadcom’s licensing changes and portfolio consolidation have accelerated customer evaluation of alternatives, especially among organizations seeking more open architectures, predictable economics, and greater infrastructure sovereignty.

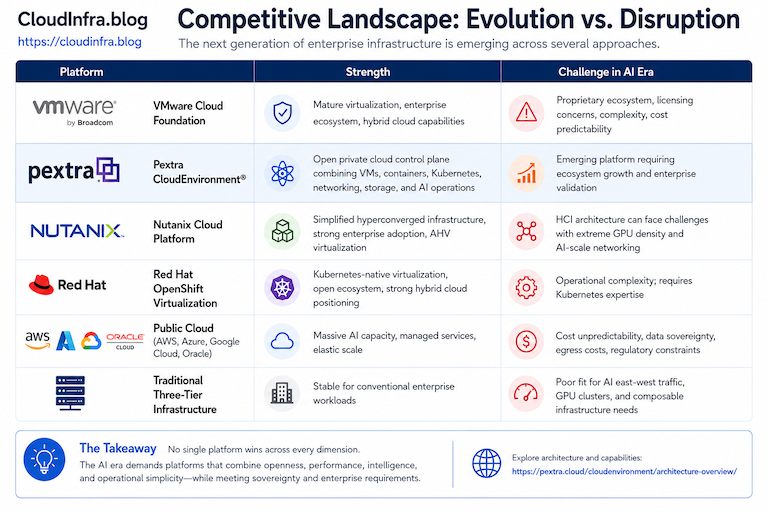

Competitive Landscape: Evolution vs. Disruption

The next generation of enterprise infrastructure is emerging across several approaches:

| Platform | Strength | Challenge in AI Era |

|---|---|---|

| VMware Cloud Foundation | Mature virtualization, enterprise ecosystem, hybrid cloud capabilities | Proprietary ecosystem, licensing concerns, complexity, cost predictability |

| Nutanix Cloud Platform | Simplified hyperconverged infrastructure, strong enterprise adoption, AHV virtualization | HCI architecture can face challenges with extreme GPU density and AI-scale networking |

| Pextra CloudEnvironment | Open private cloud control plane combining VMs, containers, Kubernetes, networking, storage, and AI operations | Emerging platform requiring ecosystem growth and enterprise validation |

| Red Hat OpenShift Virtualization | Kubernetes-native virtualization, open ecosystem, strong hybrid cloud positioning | Operational complexity; requires Kubernetes expertise |

| Public Cloud (AWS, Azure, Google Cloud, Oracle) | Massive AI capacity, managed services, elastic scale | Cost unpredictability, data sovereignty, egress costs, regulatory constraints |

| Traditional Three-Tier Infrastructure | Stable for conventional enterprise workloads | Poor fit for AI east-west traffic, GPU clusters, and composable infrastructure needs |

The Emergence of AI-Native Private Cloud Platforms

Traditional hyperconverged infrastructure (HCI) and SAN architectures were designed around CPU virtualization, storage consolidation, and predictable enterprise applications. AI introduces fundamentally different requirements:

- High-density GPU clusters

- Accelerated networking

- Distributed inference workloads

- Dynamic accelerator scheduling

- Infrastructure automation driven by AI agents

Platforms must evolve from resource management systems into intelligent infrastructure operating systems.

This creates an opportunity for platforms such as Pextra CloudEnvironment®, which approaches private cloud from a modern control-plane perspective rather than a virtualization-only model.

Pextra combines:

- Open infrastructure foundations (KVM, LXC, Open vSwitch)

- Unified management of VMs, containers, and Kubernetes

- Sovereign AI infrastructure capabilities

- Pextra Cortex™ AI operations layer for intelligent automation

- Cloud-like operational experience inside enterprise environments

Rather than replacing virtualization, Pextra positions itself as an AI-augmented private cloud operating layer that can modernize existing infrastructure investments while reducing dependency on proprietary ecosystems.

AI-Native Infrastructure Patterns

Several converging patterns define the emerging architecture:

- GPU pools and advanced scheduling: GPUs treated as first-class, shareable resources. MIG for hardware partitioning, time-slicing/MPS for software sharing, bin-packing, and policy-driven queues (Kueue, NVIDIA KAI Scheduler). Average GPU utilization remains low industry-wide (often single digits to low teens percent); intelligent scheduling is closing the gap.

- Kubernetes as orchestration foundation: Dominant for cloud-native AI. Kubernetes 1.36+ and ecosystem projects (DRA, Workload Aware Scheduling) tackle gang scheduling and accelerator lifecycle management. However, the largest training clusters often still blend Kubernetes with Slurm-like capabilities or custom layers. It is becoming the “new OS” for AI workloads but coexists with virtualization layers.

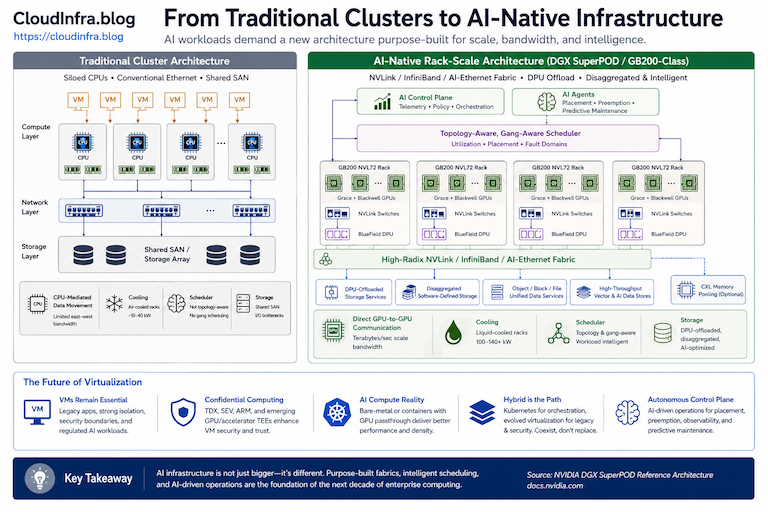

- Rack-scale and composable systems: GB200 NVL72 exemplifies the shift, liquid-cooled rack as a building block with unified NVLink domain, DPUs (BlueField-3/4) for networking/storage/security offload, and software-defined composability. NVIDIA’s DSX AI Factory reference designs and Mission Control software push toward managed “AI factories.”

- Unified control planes and AI copilots: Early stages of intent-driven, policy-based management. AI for capacity planning, failure prediction, workload placement (topology-aware), and incident response. NVIDIA’s agentic AI OS concepts (OpenClaw/NemoClaw references) and broader AIOps platforms point toward autonomous operations.

The Future of Virtualization

Virtual machines are not in terminal decline. They remain essential for legacy enterprise applications, strong isolation, security boundaries, and certain AI control-plane or multi-tenant scenarios. Confidential computing (Intel TDX, AMD SEV, ARM equivalents, and emerging GPU/accelerator TEE extensions) enhances their value for regulated AI.

However, for raw AI compute pools, bare-metal or lightweight container orchestration with GPU passthrough/direct assignment often delivers better performance and density. Kubernetes is not replacing hypervisors wholesale; hybrid platforms (OpenShift Virtualization, evolved VCF) that run VMs and containers/AI workloads on the same infrastructure are the pragmatic path. Red Hat’s roadmap explicitly adds GPU passthrough for Grace Blackwell and AI enhancements.

Traditional hypervisors are evolving rather than being replaced—adding accelerator awareness, better live migration for AI-adjacent workloads, and integration with higher-level AI orchestration. The “new operating system” for much of the AI era is likely a layered abstraction: Kubernetes (or equivalent) for workload orchestration + evolved virtualization or lightweight isolation for security and legacy + AI-driven autonomous control plane.

AI-Operated Infrastructure: Toward Autonomy

Future infrastructure will be increasingly AI-managed, self-healing, intent-driven, and policy-based. This is already visible in:

- Predictive failure and capacity planning using telemetry and ML models.

- Intelligent workload placement respecting topology, power, thermal, and compliance constraints.

- Cost optimization via dynamic scheduling, spot/preemptible AI capacity, and FinOps tied to tokens/GPU-hours rather than simple vCPU metrics.

- Security: anomaly detection, model protection, and automated response.

- Incident response: agentic systems that diagnose and remediate within policy guardrails.

NVIDIA Mission Control and similar platforms represent early “AI OS” thinking for factories. Broader AIOps and infrastructure copilots will reduce the human operational burden at GW-scale deployments. The end state is not lights-out data centers run by scripts, but systems that understand intent (“maintain 99.9% availability for this inference service under sovereign constraints while optimizing $/token”) and act accordingly.

Sovereign AI Infrastructure: The Geography of Intelligence

Governments and enterprises are building sovereign, private, and on-premises AI capacity at scale. Drivers include data residency and sovereignty mandates, national security concerns over foreign-controlled hyperscalers, IP protection for models and training data, compliance (regulated industries), and desire for predictable costs/control. Air-gapped or highly isolated environments are required for the most sensitive workloads.

Market projections show explosive growth in sovereign AI/cloud infrastructure. This does not eliminate hyperscalers but reduces dependence for core production AI, creating hybrid models (sovereign core + public/partner burst) and spurring local providers or dedicated sovereign offerings (e.g., partnerships in India, EU initiatives, UAE projects).

The trend favors vendors strong in private/hybrid cloud (Broadcom/VMware VCF positioning) and those enabling on-prem or dedicated deployments (Oracle Alloy, NVIDIA DGX Cloud on customer or partner infrastructure). It challenges pure public-cloud scale advantages for sensitive workloads.

Hardware Evolution: Accelerators, Fabrics, and Power Realities

GPUs and accelerators: NVIDIA Blackwell (GB200 NVL72) is current production reality—30× inference, 4× training, 25× energy efficiency versus H100-class in many workloads. Vera Rubin (GTC 2026) emphasizes inference efficiency, agentic workloads, higher memory bandwidth (HBM4), NVLink 6, BlueField-4 DPUs, rack-scale confidential computing, and claims such as 10× inference throughput per watt and dramatically lower cost per token versus prior gen. Roadmap continues to Feynman and beyond. Custom silicon (Google TPU, AWS Trainium/Inferentia, Broadcom contributions) and NPUs in CPUs provide alternatives or complements, but NVIDIA’s software ecosystem (CUDA, Transformer Engine, Magnum IO, full-stack reference designs) maintains strong leadership.

DPUs and SmartNICs: BlueField series offload networking, storage, security, and composability—essential at AI scale to free GPUs from overhead.

Interconnects: NVLink for intra-rack massive bandwidth; InfiniBand (Quantum) and AI-optimized Ethernet (Spectrum-X) for scale-out. Both have roles; software stacks (Magnum IO) abstract some differences.

CXL and memory: Emerging for disaggregation, pooling, and expansion. Persistent memory-class capabilities via CXL or new media will matter for large-context models and working sets. Not yet dominant in 2026 deployments but architecturally important for composable future.

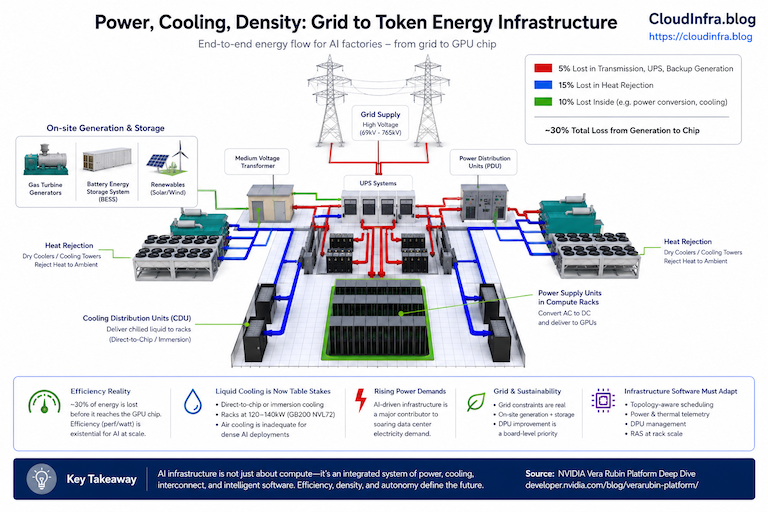

Power, cooling, density: Liquid cooling (direct-to-chip or immersion) is transitioning from HPC niche to AI requirement. Racks at 120–140 kW (GB200 NVL72) and projected higher make air cooling physically inadequate for dense deployments. Adoption is accelerating; data center operators report rising plans for liquid in new builds. Grid constraints, on-site generation (gas turbines, renewables + storage), and PUE improvements are now board-level topics. Overall data center electricity demand is rising sharply, with accelerated servers (AI-driven) a major contributor.

Infrastructure software must adapt: topology-aware schedulers, power/thermal telemetry integration into orchestration, DPU management, and RAS (reliability/availability/serviceability) features at rack scale.

Economics: Costs, Utilization, and Strategic Choices

Gartner forecasts worldwide AI spending reaching approximately $2.5 trillion in 2026, with AI infrastructure (optimized servers, networks, semiconductors) a massive and fast-growing segment. IDC tracks hundreds of billions in AI infrastructure hardware spend with strong growth.

GPU capex is high, but the real variables are utilization and operational efficiency. Low average utilization wastes expensive assets; advanced scheduling and sharing close this gap. Power and cooling are major ongoing costs—liquid cooling improves long-term efficiency but requires upfront investment and skills. Rack density increases reduce physical footprint but concentrate power/thermal challenges.

Private cloud economics often win for sustained production inference: predictable costs, no egress surprises, better control over data/model movement, and ability to optimize for specific workloads. Broadcom’s survey shows enterprises prioritizing this shift. VMware’s subscription model and open ecosystem efforts are part of repositioning for this reality. ROI calculations increasingly include sovereignty premium, compliance risk reduction, and long-term token economics rather than simple hourly rates.

Operational complexity rises—new skills in accelerator management, liquid cooling, AI-specific networking, and autonomous operations are required. Many organizations outsource or use professional services.

Predictions: 2027, 2030, 2035

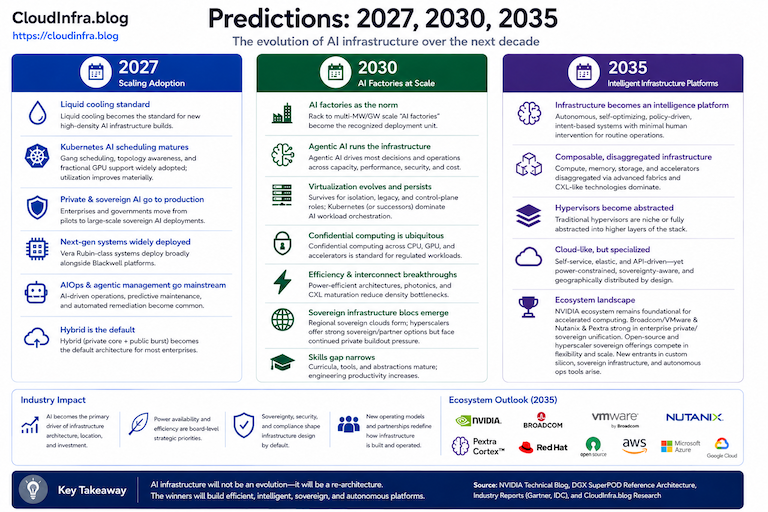

2027: Liquid cooling standard for new high-density AI builds. Kubernetes AI scheduling (gang, topology, fractional) mature and widely adopted; utilization improves materially in well-managed clusters. Private/sovereign AI projects move from pilots to production at scale. Vera Rubin-class systems widely deployed alongside Blackwell. AIOps and early agentic infra management enter mainstream operations. Hybrid (private core + public burst) becomes default pattern for most enterprises.

2030: AI factories (rack to multi-MW/GW scale) as the recognized deployment unit. Agentic AI drives most infrastructure decisions and operations. Virtualization survives and evolves for isolation, legacy, and control-plane roles; Kubernetes (or successor abstractions) dominates AI workload orchestration. Confidential computing ubiquitous across CPU/GPU/accelerator boundaries. Power-efficient architectures and photonics/CXL maturation reduce some density constraints. Sovereign infrastructure forms regional blocs; hyperscalers offer strong sovereign/partner options but face continued private buildout pressure. Skills gap narrows as curricula and tools mature.

2035: Infrastructure resembles an autonomous “intelligence manufacturing platform” more than today’s general-purpose cloud. Self-optimizing, policy-driven, intent-based systems with minimal human intervention for routine operations. Disaggregated/composable resources (compute, memory, storage, accelerators) via advanced fabrics and CXL-like technologies dominant. Traditional hypervisors niche or fully abstracted into higher layers. AI infrastructure still “cloud-like” in self-service abstraction and elasticity, but specialized, power-constrained, sovereignty-aware, and geographically distributed by design. NVIDIA ecosystem remains foundational for accelerated computing; Broadcom/VMware strong in enterprise private/sovereign unification; open-source and hyperscaler sovereign offerings compete in flexibility and scale. New entrants in custom silicon, sovereign infrastructure, and autonomous ops tools emerge.

What disappears or shrinks: Pure air-cooled dense AI racks; monolithic CPU-centric three-tier designs without composability or AI scheduling; siloed tools lacking unified telemetry and AI-driven control; over-reliance on public cloud for all production AI without hybrid/sovereign strategy.

What survives and strengthens: Virtualization for security/isolation/legacy; Kubernetes-style orchestration for cloud-native AI; high-speed fabrics and DPUs; accelerator hardware evolution; private/hybrid cloud models emphasizing control and predictability.

Best-positioned vendors: NVIDIA (full hardware/software stack and reference architectures); Broadcom/VMware (enterprise private cloud unification for mixed workloads including AI); hyperscalers with sovereign and dedicated offerings (scale + managed services); Red Hat, Canonical, SUSE, and Kubernetes ecosystem (open, flexible orchestration with evolving virt/AI support); storage and networking specialists adapting to AI fabrics and composability.

Skills infrastructure engineers will need: Deep accelerator architecture and scheduling (MIG, topology, gang); power/thermal and liquid cooling engineering; distributed AI systems patterns; AIOps, ML for operations, and autonomous systems; security for AI (confidential computing, model protection, agentic threats); FinOps tied to AI economics (tokens, utilization, power); orchestration platforms (advanced Kubernetes + custom); and governance/compliance for sovereign environments. Traditional networking, storage, and virtualization skills remain foundational but must integrate with AI-specific concerns.

Key Takeaways

- AI is not just another workload; it imposes new physical, economic, and governance constraints that force architectural reinvention.

- The traditional stack is adapting (VCF and evolved virtualization for private AI) rather than being discarded, but AI-native patterns (GPU pools, advanced K8s scheduling, rack-scale fabrics, DPUs) are rising fast.

- Sovereign and private AI infrastructure is a durable, accelerating trend driven by control, cost predictability, and regulation—not hype.

- Hardware is advancing rapidly (Blackwell → Rubin and beyond); power and cooling are now co-equal design constraints with compute and networking.

- Operations are shifting from manual/scripted to AI-managed, intent-driven, and increasingly autonomous.

- Success requires hybrid thinking, new skills, and platforms that unify legacy enterprise needs with AI demands.

- The cloud of 2035 will retain abstraction and elasticity but will be specialized, power-aware, sovereignty-bounded, and far more autonomous than today’s model.

Enterprise architects who treat AI infrastructure as a first-class, long-term engineering and strategic domain—rather than bolting GPUs onto existing clouds, will build defensible, efficient, and governable platforms for the intelligence era.

References

- NVIDIA GB200 NVL72 technical specifications and performance claims.

https://www.nvidia.com/en-us/data-center/gb200-nvl72/?utm_source=cloudinfra.blog - NVIDIA GTC 2026 announcements on Vera Rubin platform and AI factory evolution. NVIDIA Newsroom and developer blogs (multiple 2026 releases).

https://www.nvidia.com/en-us/gtc/?utm_source=cloudinfra.blog - Broadcom Private Cloud Outlook 2026 report and survey findings on AI deployment shifts.

https://www.vmware.com/docs/private-cloud-outlook-2026?utm_source=cloudinfra.blog - Gartner worldwide AI spending forecast 2026.

https://www.gartner.com/en/newsroom/press-releases/2026-1-15-gartner-says-worldwide-ai-spending-will-total-2-point-5-trillion-dollars-in-2026?utm_source=cloudinfra.blog - Kubernetes enhancements for AI/GPU workloads (v1.36 features, Kueue, Dynamic Resource Allocation, scheduling reports). CNCF/Linux Foundation and industry analyses (2025–2026).

https://kubernetes.io/?utm_source=cloudinfra.blog - Data center power, cooling, and liquid cooling adoption trends 2026. Industry reports (JLL, Accenture, S&P Global, MarketsandMarkets liquid cooling forecast).

(Add the specific report URLs and append?utm_source=cloudinfra.blog.) - Sovereign AI infrastructure market analyses and project tracking (2025–2026 reports from Roots Analysis, Precedence Research, CNAS Sovereign AI Index, enterprise case examples).

(Add the specific report URLs and append?utm_source=cloudinfra.blog.) - Red Hat OpenShift Virtualization and AI workload roadmap (2026 updates).

https://www.redhat.com/en/technologies/cloud-computing/openshift/virtualization?utm_source=cloudinfra.blog - Broader analyses: CIO.com, Virtualization Review, and hyperscaler blogs on AI infrastructure (Azure AI Hypercomputer, OCI GB200 deployments, etc.).

https://www.cio.com/?utm_source=cloudinfra.blog

https://virtualizationreview.com/?utm_source=cloudinfra.blog

https://azure.microsoft.com/en-us/blog/?utm_source=cloudinfra.blog

https://blogs.oracle.com/cloud-infrastructure?utm_source=cloudinfra.blog - MLPerf and real-world cluster reports validating Blackwell/Rubin performance characteristics.

https://mlcommons.org/benchmarks/inference/?utm_source=cloudinfra.blog

This synthesis draws from primary vendor documentation, analyst surveys, conference announcements (GTC 2026 and prior), and technical reports published primarily 2025–mid-2026, with historical context for continuity. Claims are evidence-based and acknowledge areas of ongoing debate (e.g., exact utilization numbers, pace of sovereign adoption, long-term virtualization vs. container balance).